There has been much discussion of the future contribution of artificial intelligence to increased economic productivity and, hence, rising income growth — and that higher incomes would lower the federal budget deficit through increased tax revenues. This mechanism appears to be a significant part of the Trump administration’s calculations in positing a future annual rate of real gross domestic product growth of 3%, compared to the 2% others assume and most recently experienced. Along with higher tariffs and assumed lower interest rates, this leads the administration to project a halving of the deficit over 10 years rather than doubling.

Recent compelling independent economic research suggests that AI can raise productivity growth over the next 10 years by 0.9 percentage points from its current rate of about 1.8% to 2.7% — essentially a 3% GDP growth rate when modest labor force growth is added.

Recommended Stories

More thorough consideration of the broader implications of this productivity jump, however, leads to the opposite budget result. Absent a change in fiscal and healthcare policy, the deficit, currently around 6% of GDP, will continue to increase and even deepen. Higher productivity, while raising incomes, also raises interest rates and, therefore, federal interest spending, given high debt levels. It also raises the prices of, and demand for, services in the inefficient healthcare sector, and therefore government spending on Medicare, Medicaid, health exchanges, veterans’ health benefits, and so on. A run of my economic growth, healthcare, and budget model shows that these spending increases more than swamp rising tax revenues.

The model is, in one respect, a conventional growth model, in which national income results from the application of capital (arising from saving) and labor (arising from worker demographics) to the production of goods and services, with productivity growth enhancing wages and income. Productivity, though, requires large amounts of scarce capital to be realized, as demonstrated increasingly by data centers and other IT infrastructure.

An increase in productivity therefore bids up the cost of capital and interest rates, including what the federal government must pay on its debt. Distinctively, this model includes the separate healthcare sector, on the grounds that it is significant — currently over 18% of GDP — and because it is inefficient. Research shows it has a very low rate of productivity improvement. This explains why the cost of healthcare rises faster than that of other goods and services, combined with consumers’ relatively low-price sensitivity and demand that grows with rising income and an aging population, almost universally covered by private and public insurance.

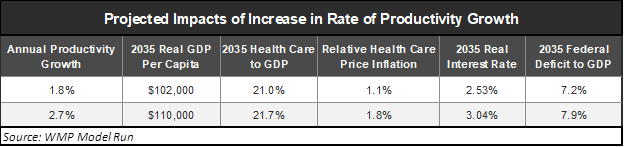

The model includes a full delineation of the federal budget, covering discretionary spending (defense and general government), mandatory programs (Social Security, Medicare, Medicaid, and so on), income and payroll taxes, and interest payments. It uses current demographic projections, which are critical to long-run results owing to the aging population’s effect on labor force growth, healthcare demand, and Social Security payouts. See model projection results in the table below.

Currently, GDP per capita is about $87,000. With annual productivity growth of 1.8%, based on historical averages, this welfare measure for the U.S. population will grow to $102,000 by 2035. With productivity rising to 2.7%, per capita income is projected to reach $110,000, a clearly positive result for welfare.

Currently, healthcare spending is 18.3% of GDP. With 1.8% productivity growth in the broad economy but not in the healthcare sector, which has been slow to adopt AI, and an aging population, the health spending-to-income ratio is projected to rise to 21% of GDP by 2035, with relative healthcare inflation running at 1.1% annually. When productivity increases to 2.7%, health prices rise more rapidly at 1.8% annually, pushing spending to 21.7% of GDP.

Currently, real interest rates on government debt are around 2.2%. With large deficits and growing debt, the real interest rate is projected to rise to 2.53% in 2035 under current productivity. If productivity increases, the real interest rate reaches 3.04%.

DON’T LET GOVERNMENT PICK WINNERS AND LOSERS ON AI

The combined result of these impacts, considering the government covers about half of healthcare spending and that debt outstanding now equals GDP, is that the federal deficit ratio, currently around 6% of GDP, worsens to 7.9% rather than the 7.2% projected under lower productivity growth. Moreover, these effects grow larger past the ten-year horizon.

While the AI revolution will benefit economic performance, it is not a savior for the worsening federal fiscal situation; to the contrary, it deteriorates matters further. There is no substitute for the hard work of improving healthcare productivity through market competition and consumer cost sensitivity, alongside prudent fiscal policy.