Once again, it seems, the federal government stands at the edge of a pending debt crisis. According to recent estimates, even while the nation enjoys the longest uninterrupted economic expansion in memory and unemployment hovering at bargain basement levels, our national addiction to red ink-funded government spending means the Treasury could run out of cash in September.

The Treasury Department could creatively shuffle money across its many accounts and find additional spending power as a brief and temporary fix. Eventually, Congress will either raise the debt limit again, face another government shutdown, or allow the United States to become another member of that notorious set of countries that have defaulted on their debt.

Recommended Stories

But, be not afraid. Yes, we may get a temporary fix or even another shutdown, but we will not default on our debt — yet.

The cash shortfall warning arrived with Congress struggling to pass a budget while preparing for the usual August recess, leaving little time to deal with this apparently important fiscal problem and address a long list of other Washington-concocted crises. Of course, our entire legislative and executive branches were not asleep at the switch; they knew the day of reckoning was on its way and could have, one would think, taken quiet and effective action sooner.

But alas, what passes as common sense in managing a household comes across as nonsense in Washington. Instead of quietly fixing things, politicians love crises, especially those they can orchestrate, control, and exploit.

Here we have another made-in-Washington crisis which, like all such concoctions, is an opportunity for evening news bombast and speeches with dire warnings about our spendthrift ways. Until finally, a just-in-time solution will keep Uncle Sam in business for yet another few quarters.

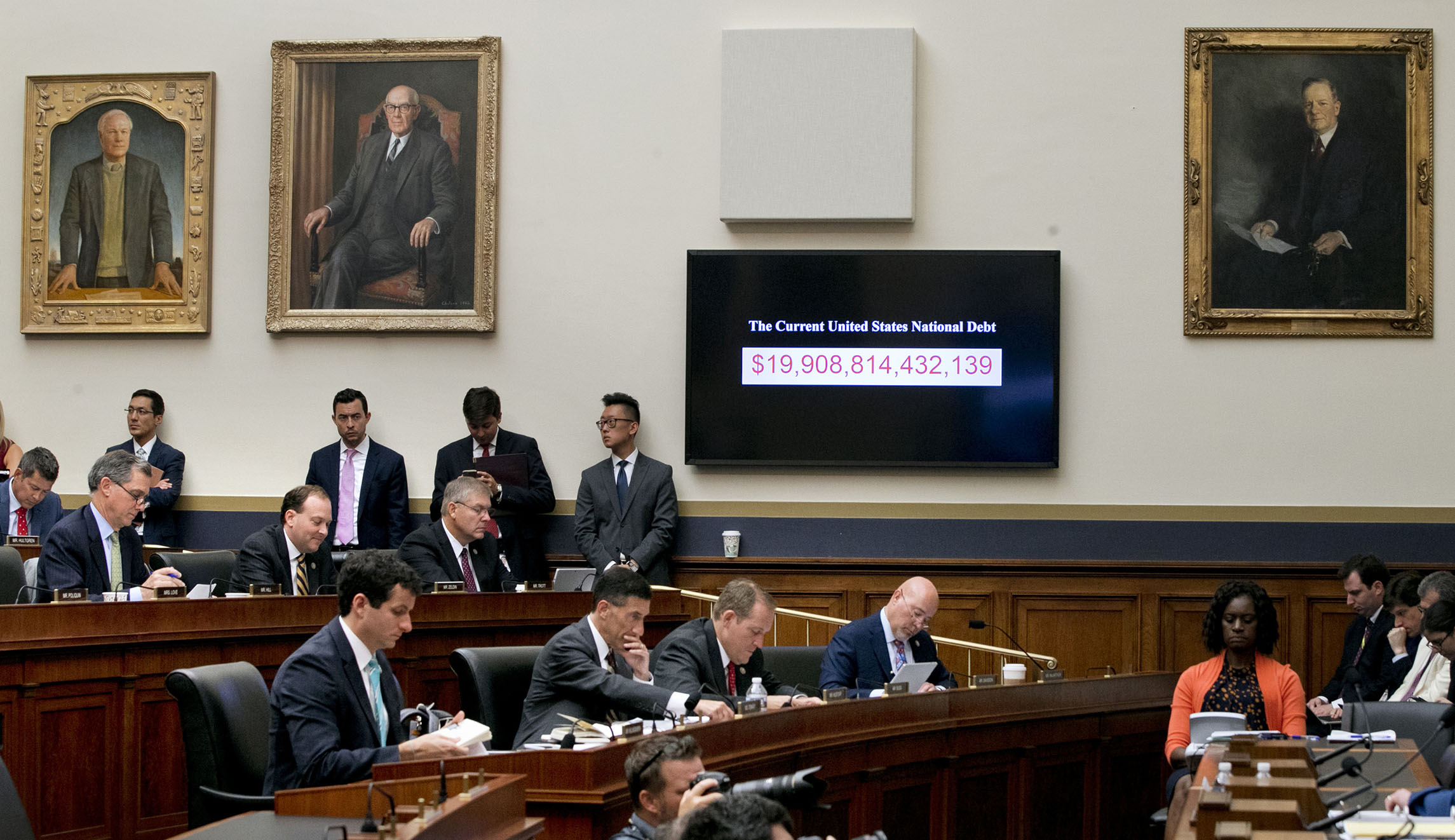

The government has hit and raised the debt limit 78 times since 1960, some 49 under Republican administrations and 29 under Democrats. That’s almost 60 years of repeating boom-to-bust federal purse management, yet we still get caught short-handed on a regular basis. Why?

In their 1998 book, Democracy in Deficit: The Legacy of Lord Keynes, Nobel Laureate James M. Buchanan and his colleague Richard E. Wagner applied “public choice” concepts to explain seemingly perpetual deficits and why, in a democracy, it is so difficult to do anything about them. As the two scholars suggest, it’s not rocket science.

Here’s how the story goes: Democratically elected officials do what they can to please voters back home and keep their jobs. Predictably, voters back home love government benefits and hate taxes. So, successful politicians work the fiscal switches accordingly, expanding benefits and funding them with debt, not taxes. Citizens observe a lower tax-price for desirable government-provided benefits. The lower price prompts calls for more government activity and therefore more deficits and debt.

Issuing more debt is not the only way to provide seemingly bargain-priced government benefits. Governments can also just print money or, as we now say more politely, engage in quantitative easing. Printing money and issuing debt can generate inflation, but the folks back home have no easy way to make the connection between more Washington goodies and higher grocery store prices.

The dual ability to borrow and to print money yields a situation that causes some to think our nation should just open the valves even more, expanding government-provided benefits and services almost without limit. Other, more cautious souls suggest a day of reckoning will come when interest rates rise and the interest cost of debt becomes unbearable. For now, we get more frequent encounters with debt ceilings.

But the incentive to borrow and inflate doesn’t explain the need to do so through political crises, chaos, and last-minute congressional fiscal hassles. The answer has to be that politicians like it the way it is.

Chaos and crises require last-minute action. That provides opportunities to pack pork into the resulting remedy legislation, since there will be little time for debate and fiscal house cleaning. Even the remedy itself leads to more spending, more debt, and an expanded government. So fasten your seatbelt and get ready to observe the management of next debt ceiling crisis.

Bruce Yandle is a contributor to the Washington Examiner’s Beltway Confidential blog. He is a distinguished adjunct fellow with the Mercatus Center at George Mason University and dean emeritus of the Clemson University College of Business & Behavioral Science. He developed the “Bootleggers and Baptists” political model.