The first open enrollment for Obamacare starts Nov. 1 without its architect and chief advocate in the White House, raising questions about how it will fare under a new administration that views repeal of the law as one of its main priorities.

When former President Barack Obama was in office, he openly worked to sell plans on the law’s exchanges and to fund the law, sometimes issuing decisions beyond what his critics considered were allowable under presidential authority.

Recommended Stories

During his first open enrollment in 2014, Obama targeted young people by appearing on the comedy interview show “Between Two Ferns” with Zach Galifianakis, soon after the federal exchange website, healthcare.gov, failed to launch properly. By his last open enrollment, he doubled ad funding from $50 million to $100 million.

Obama oversaw three open enrollment seasons. During that time he made numerous administrative moves to ensure Obamacare’s success, such as delaying the end of open enrollment several times, creating special enrollment periods for people to sign up outside of the designated timeframe, and propping up smaller insurers called co-ops. He allowed people to sign up for plans that did not comply with Obamacare’s mandates and authorized insurer funds known as cost-sharing reduction subsidies, a move that a federal judge ruled illegal because they weren’t appropriated by Congress.

Obama’s departure, and subsequent arrival of an administration not as interested in the law’s success, leaves open the question of whether Obamacare can succeed without a massive lift from the White House.

The law struggled despite Obama’s actions. A sicker-than-expected risk pool caused by not enough younger and healthier people signing up contributed to hundreds of millions of dollars in losses for most insurers in the exchanges, leading to exits and price increases for 2017.

Those struggles have fallen into the lap of the Trump administration, which spent most of the year trying unsuccessfully to repeal much of Obamacare. Repeal efforts collapsed in the Senate and are on hold while the Republican-controlled Congress tries to pass tax reform.

The Trump administration is in an awkward position: It has to carry out 2018 open enrollment under Obamacare after months spent working with Republicans in Congress trying to unwind it.

Critics, including Obama administration veterans, have seized on nearly every action by the Trump administration as evidence that it is trying to “sabotage” the law.

“I think the Trump administration can be very successful in damaging this law if they want,” said Andy Slavitt, who was acting director of the Centers for Medicare and Medicaid Services under Obama. “They want to be able to say that this is a horrible law and the American public doesn’t want it and you look at these enrollment numbers.”

The president has given them plenty of political ammunition. Trump has said on Twitter that he wants to let the law “implode.” He signaled from the beginning of his presidency that his administration would not deliver the kind of support that Obamacare relied on, signing an executive order on his first day in office that called for federal agencies to ease any financial burdens from the law.

Trump’s health officials have made it no secret that they believe the law is collapsing. They have routinely sent out news releases highlighting premium increases or a major insurer leaving a state, emphasizing the collapse of the law that they are tasked with running.

News about the first Trump-run open enrollment has trickled out. The timeline for enrollment would be shorter, the funds spent on advertising and navigators smaller, and senior officials said they no longer planned to make visits to states to participate in promotional events. The site would be down during open enrollment for as many as 12 hours nearly every Sunday from midnight to noon for scheduled maintenance.

More recently, Trump signed an executive order to direct agencies to loosen Obamacare’s insurer regulations and abruptly announced that his administration would no longer fund the insurer payments that a judge had ruled illegal under Obama.

“Obamacare is dead,” Trump said at the White House shortly after issuing his decisions in early October. “There is no such thing as Obamacare anymore.”

The administration’s actions are “certainly not helping,” Jennifer Tolbert, director of State Health Reform at the Kaiser Family Foundation, said during a webinar about open enrollment. “What we know is that consumers need to hear this information over and over again.”

She added that any cuts to marketing may mean that fewer customers will hear messages about open enrollment or be aware of deadlines.

Not everyone agrees that Trump’s actions have as much weight as Obama-era officials say, noting that Obamacare gives wide discretion to the executive branch in implementing the law. The Trump administration has said that the government spent $62.5 million under Obama on navigators, which ultimately enrolled 81,426 individuals, a small fraction of the 12.7 million on the exchanges in 2017.

Tevi Troy, CEO of the conservative Health Policy Institute, doesn’t believe the changes to the awareness campaigns will have as much as an effect as factors such as affordability and whether people value the plans.

“Would navigator dollars lead people to purchase a product they don’t want? That is inherently the problem with the exchanges,” Troy said. “But at the end of the day it’s hard to get people covered. Part of this inability is that customers don’t think they’re getting a good deal.”

He also disputes the conclusion of critics who say that if enrollment doesn’t rise, it’s because of “sabotage.” He notes the cost-sharing payments, for instance, were ruled illegal under Obama.

“There are a lot of other factors involved,” he said. “The Obama administration did everything it could to prop it up, including taking an extreme interpretation of the discretion they were given. I don’t think it is fair to say that not engaging in the same kinds of overreach that the Obama administration engaged in should be considered sabotage.”

Trump administration officials also pushed back on claims of “sabotage” in an interview with the Washington Examiner.

“None of those decisions were made because we were trying to sabotage Obamacare but because we decided they were the best policy decisions,” a senior health official said.

Trump’s open enrollment: ‘Functional’

For this year’s open enrollment, which starts Wednesday, customers will have fewer options for health insurance coverage than last year and people who do not receive subsidies to pay for premiums will face higher costs.

Amid continued losses and the uncertainty over whether to expect cost-sharing payments, insurers grew anxious about the viability of the exchanges and began to pull out. Those that stayed requested double-digit rate increases on the premiums of middle-level plans, known as silver plans.

The Trump administration estimates that more than half of U.S. counties will have only one insurer next year, which will affect 30 percent of people who buy coverage through healthcare.gov.

When asked about whether the Trump administration wanted Obamacare to be successful, an administration official said earlier this year it wanted the exchanges to be “functional.”

The Department of Health and Human Services allowed Obamacare customers to begin to “window shop” on healthcare.gov a week before open enrollment. They also staffed the call center at the same level as the year before and are making brokers and agents available to help people sign up for plans, rather than relying on navigators. Additional changes include allowing people to sign up for coverage while still receiving subsidies through websites other than healthcare.gov.

A senior health official said that the Department of Health and Human Services was “implementing open enrollment according to the law.”

“We are making people aware of how and where to sign up,” the official said.

But administration officials did not set a target for this year’s enrollment, as the Obama administration did.

“Our target this year is to have a seamless open enrollment for consumers,” said Randy Pate, deputy administrator for the Centers for Medicare and Medicaid Services. “That’s what we are focused on. The numbers we think will take care of themselves.”

It could be that Obamacare enrollment has plateaued, no matter who is in the White House.

“The exchange enrollment has never gotten up much above 10 million people,” said Joseph Antos, a fellow at the conservative think tank American Enterprise Institute. “What I think is likely to happen is that whether they want to call it sabotage or not, this is a program at least in terms of the exchange population that was never gonna grow or get bigger.”

He said growth was always going to be hampered by dramatically rising premiums for unsubsidized enrollees. And those increases started before Trump entered the White House.

Antos predicts enrollment could drop from about 10.3 million people to 9 million.

“I would expect a little bit of shrinkage but not catastrophic shrinkage,” he said. “There isn’t going to be a lot more people joining the exchange plans. I would have said that before this year.”

Antos said that there could be a change if the plans are better or cheaper for consumers and they can pick the physician they want.

He predicted the future of Obamacare’s exchanges to be a graduate Medicaid program that most likely could be used by people who would take advantage of the subsidies.

But Antos said that doesn’t mean that some of the moves Trump is making isn’t having an impact on the market. He pointed to the decision to end cost-sharing reduction payments.

If Congress does nothing about the payments and does not make other changes to Obamacare, the exchanges will continue to function, but by shifting costs to the federal government and to middle-income people who buy Obamacare plans.

Insurers were prepared for Trump to end the payments because he had said that he was considering it. The payments help low-income Obamacare customers receive discounts to pay for out-of-pocket medical costs. Insurers still must offer them under the law and will raise premiums to recoup the costs.

Low-income people are shielded financially from the increase in the costs of premiums because the federal government offers them another type of subsidy to pay those expenses. According to Kaiser Family Foundation data, about 8.7 million people receive those subsidies. Still, doing so results in more spending by the federal government. A Congressional Budget Office analysis found it would spend as much as $194 billion over a decade in premium subsidies.

The premium increases also affect people who make more 400 percent of the poverty line, meaning more than $48,240 a year for an individual or $94,400 for a family of four, the income at which people aren’t eligible for premium subsidies. About 6.7 million people fall into that category, and most of them buy plans off the exchange, such as directly from an insurer. The plans still must abide by Obamacare’s rules and are therefore more expensive. Avalere Health, a consulting firm, concluded in a recent analysis that some customers may choose not to buy Obamacare plans, and more people could become uninsured.

Insurers in some states are shifting premium increases only onto silver plans, which means that Obamacare shoppers could gravitate toward bronze or gold plans that will be less expensive than silver, some experts say. A bronze plan covers fewer benefits than silver and a gold plan covers more, but with the boost to silver plan costs, they might provide better options, as long as people know what to look for.

“People who make more than 400 percent of poverty line really need to shop around and spend serious time on trying to figure out what the best option is. There are scenarios where they won’t be worse off than they normally would be,” said David Anderson, a research associate at Duke University’s Margolis Center for Health Policy.

Jonathan Gruber, an MIT economist who helped write Obamacare, notes that Trump’s decision to end the payments causes care for sicker Americans to become more expensive. Those with pre-existing illnesses who depend on regular care are most likely to sign up for Obamacare plans regardless of what the Trump administration does. And people who receive subsidies to pay for premiums, who will be shielded from rate increases because the government kicks in more to help out, are likely to do the same.

“The first rule of health insurance is that the sick sign up first,” Gruber said. “For the sick, health insurance in a necessity. It needs to be sold to the healthy. They have to understand why it’s in their interest to buy it.”

“For people buying on the exchange, either they are paying higher premiums or the government is paying higher premiums on their expense,” Gruber continued. “No one is winning from these decisions … [Trump] is only creating losers.”

Obama administration veterans have seized on those examples, saying that the Trump White House has been trying to sabotage the law.

They also shared another anecdote.

Before Obama left office, his administration put together a playbook to ensure a smooth transition for operating Obamacare. It contained information about the best way to conduct outreach, including that they found the top driver of awareness about enrollment was through TV ads.

“It was something that we thought about a lot … wanting to make sure that no matter who became president, whether Republican or Democrat, that we had left the marketplace in a good place,” said Lori Lodes, who ran Obamacare outreach during the law’s second and third open enrollment.

But Lodes was surprised at what happened after Trump came in, cutting $5 million in Obamacare TV ads.

“They have taken this information and used it as almost a playbook on how to undermine the law,” she said.

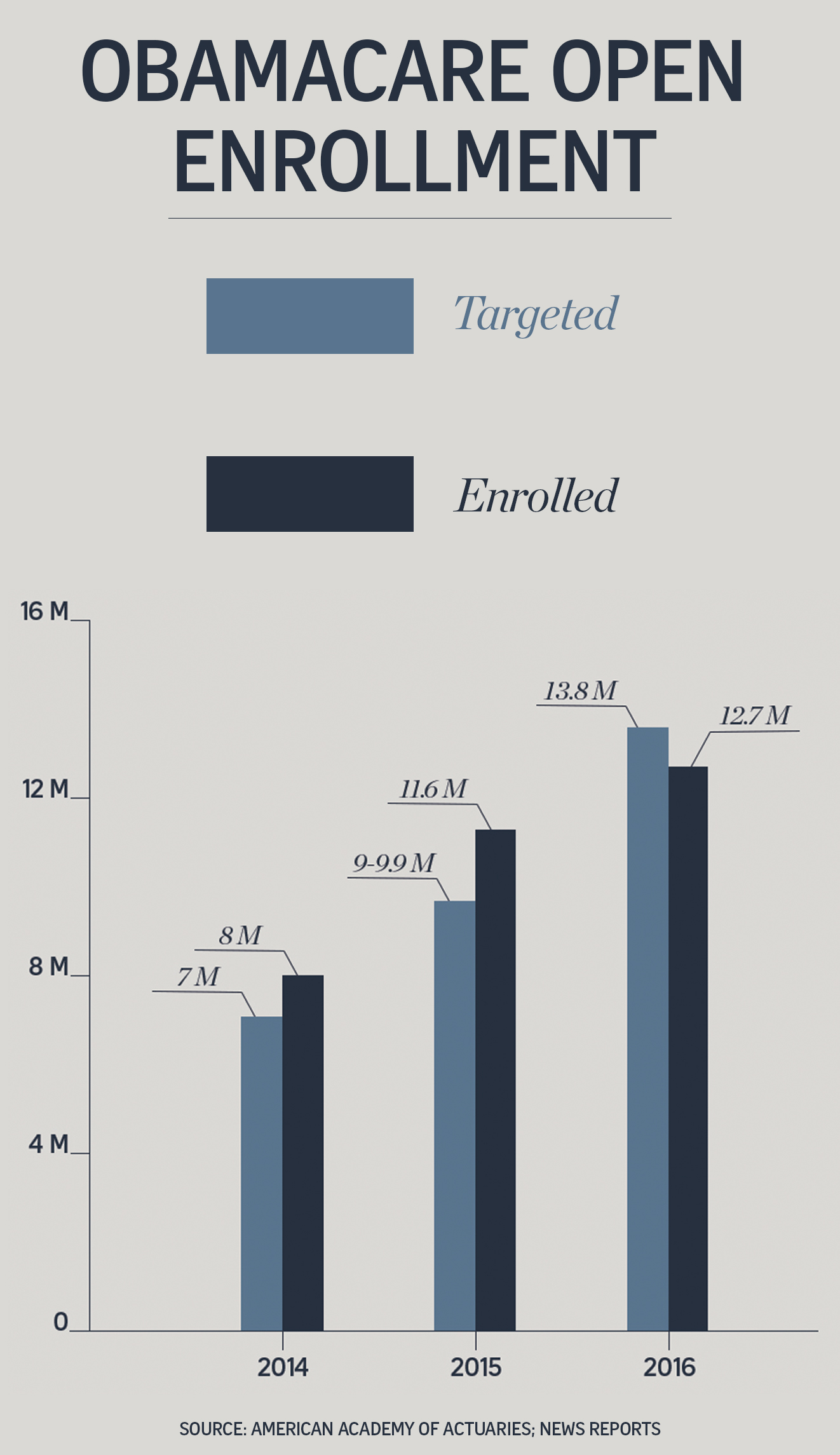

Last year the Obama administration set a goal of 13.8 million people signing up but ended up enrolling about 12.7 million, a result former officials blamed on the Trump administration pulling the TV ads. As of March, about 10.3 million people paid their Obamacare premiums.

The Obama administration surpassed its enrollment targets in the first two years, though it extended the deadlines both years and set its target lower the second year than the Congressional Budget Office had projected. Ultimately enrollment fell far short from what CBO projected in 2013, when it said enrollment would reach 24 million by 2016.

This year, outside groups are trying to fill the hole left by the Trump administration in terms of outreach, but their efforts illustrate the problems with running Obamacare without administrative support.

“The government was able to put in significant resources that is not just money for ads,” said Lodes, who set up the Obamacare outreach group Get America Covered with former Obama veteran Josh Peck. “We had a big team who was very focused on every day figuring out how to help consumers get coverage. That is not happening now. There is not that huge team on the outside.”

Lodes added they don’t have access to the same information the federal government has.

“The government has the e-mail list that we built,” she said. “We were able to have a direct conversation with 20 million people about getting coverage.”

‘You break it you buy it?’

The troubles in the exchanges precede Trump. Only weeks before he would be elected president, the former administration announced that Obamacare’s silver plans would rise on average by 22 percent nationwide, and many major insurers announced they would no longer be providing coverage following millions of dollars in losses.

“It’s important to remember that Obamacare enrollment was in decline before President Trump took office,” said Matt Lloyd, spokesman for Health and Human Services. “The previous administration inflicted heavy damage on the individual market – premiums doubled, insurers dropped out of the individual market in droves, millions of Americans saw their plans canceled because Washington didn’t approve of them, and millions more paid billions in fines to avoid the kind of coverage Obamacare dictated. That’s not evidence of a healthy, competitive market nor one that is best serving individuals and families.”

Some analyses have argued that increases in previous years were part of a one-time correction, saying that insurers priced initial plans too low because of uncertainty over who would sign up for the marketplace. Still, insurers for the most part have continued to amass losses in 2017, according to quarterly earnings reports from insurance companies.

Ahead of the midterm elections, news about the next open enrollment will surface again. If the law continues to struggle, more headlines will carry news of rising premiums and insurer exits.

“The $64,000 question is: Who gets blamed?” Gruber said, referring to the midterm elections. “Any objective observer would see it is clear that Trump has made things worse. The thing is, will voters see it that way?”

According to an August poll by the Kaiser Family Foundation, 60 percent of voters said that because Trump and Republicans are in control of the government, they are responsible for any problems with Obamacare, more than double the number who place the responsibility on Obama and Democrats.

“I think that if they break it they will own it,” Lodes said. “I think that could cause them to rethink some of their actions if they hear loud and clear that people aren’t going to stand for playing politics with their healthcare.”

But Gruber admitted that he doesn’t know anymore what the effect on voters will be after being surprised by Trump’s victory.

“The Affordable Care Act will totally survive,” Gruber said, using the formal name for Obamacare. “But it’ll survive in a form where it looks more and more like a government program and less like private insurance.”

Troy agreed that Obamacare was not in its “do or die” year.

“As long as you have a big government entity with a market it is going to fund, then the provisions are going to exist until Congress tells it to change.”

Many Republican lawmakers say they want to take up Obamacare repeal again, likely in 2018, but that would mean taking up a contentious bill during an election year. Meanwhile, more Democrats are latching onto an effort from Sen. Bernie Sanders, I-Vt., to create a government-run healthcare program.

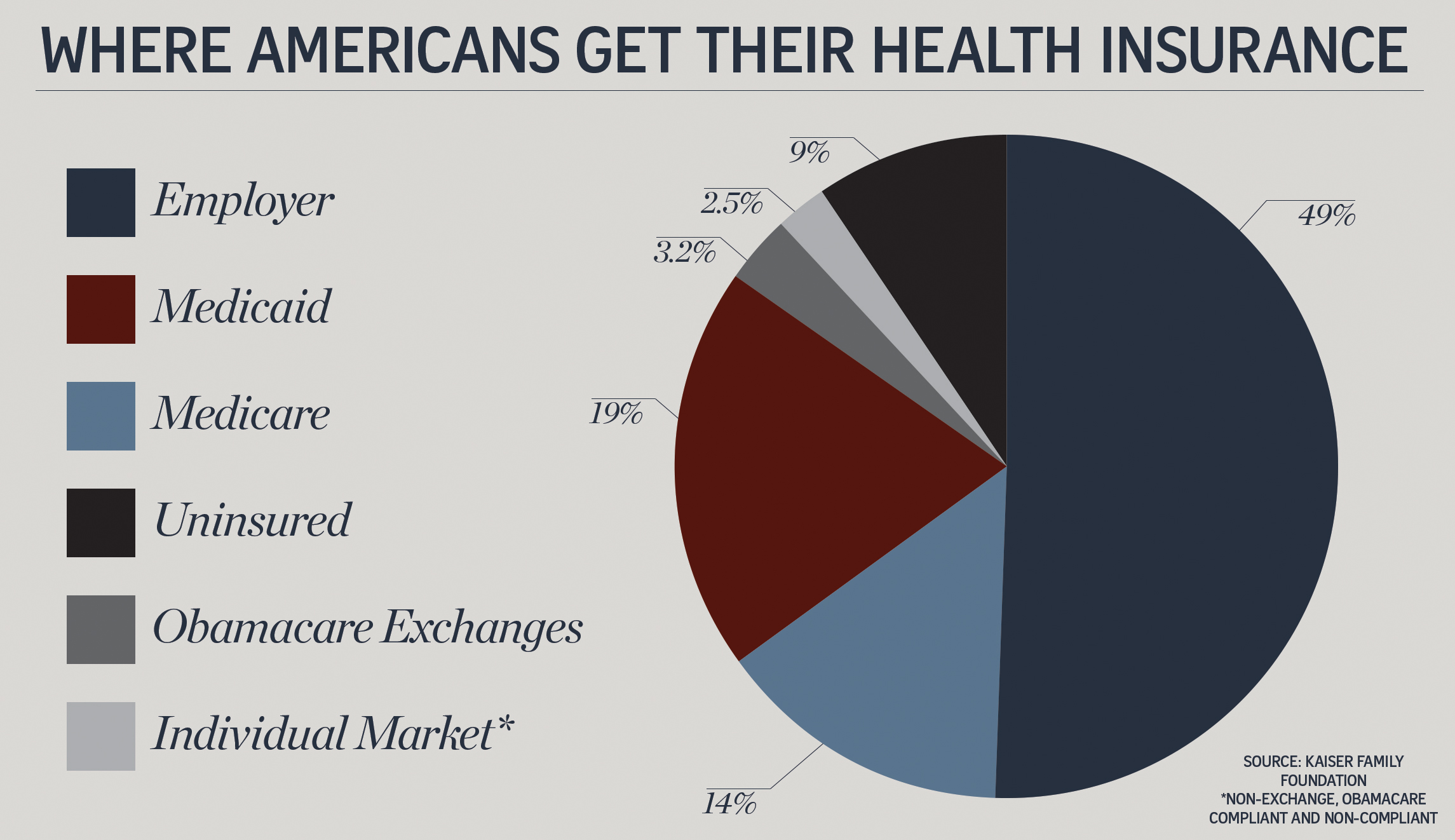

Complicating a prediction about how issues with Obamacare’s exchanges could affect the election is that most voters mistakenly believe that Trump’s actions on Obamacare customers affect them. A recent Kaiser Family Foundation poll showed that nearly 60 percent of people believe everyone who buys health insurance will be affected if insurers decide not to sell Obamacare plans. In reality, the decisions affect the roughly 6 percent of people who buy their own health insurance, not the majority of those who receive coverage through government programs or through their employers. About half of the people who buy health insurance on their own, or 3.2 percent of the population, buy it through the exchanges.

Still, that reality doesn’t offer much reassurance to customers who enroll in the plans, who make too much to qualify for subsidies and cannot forego insurance because of a pre-existing illness. They are facing the prospect of paying much more for health insurance coverage next year.

Because so many insurers have left, even customers who do receive subsidies are facing disruption heading into 2018. The plans they will be offered may not have a doctor in their network who they have been seeing for years or may only cover a hospital that is further away. Patients in the middle of treatment face the prospect of shifting all their medical care elsewhere.

The misunderstanding of the law, coupled with real difficulties that as many as 16 million customers will face, can allow both sides to seize on the results this year and next to advance their narratives.

“I think there will be a blame game and finger pointing on all sides,” Troy said. “Republicans will have a good point saying, “You passed this and it’s not working great, and Democrats will say, ‘It was working great until they came along.'”

Republicans, he said, will have more difficulty making their case because they are the party in charge.

“I think Republicans have a double challenge in that the Democrats will say, ‘It’s your fault,’ but second, Republicans also didn’t do anything legislatively to change it,” Troy said. “It’s hard for Republicans to navigate the reality that, ‘This thing isn’t working and you’re in charge, and you didn’t do anything to fix it.'”

Some Republicans have expressed openly that they believe they will be blamed for Obamacare’s troubles.

“President Trump is the president. He is a Republican. And we control the Congress. We own the system now,” Rep. Charlie Dent, co-chairman of the centrist Tuesday Group, said recently on CNN. “Barack Obama is no longer in the equation. So this is on us.”

Sen. Lindsey Graham, R-S.C., echoed similar sentiments.

“If we can’t repeal and replace Obamacare, why have us up here?” Graham said on Fox News. “If we do not deliver, we are going to disintegrate as a party, and we will have no one to blame but ourselves.”