Fragile by Design is James Madison for depressives—and he’s even a protagonist. Charles Calomiris and Stephen Haber argue that states are essential for banking systems (and vice versa) and that rent-seeking bargains drive their joint structure. No mere reverse Panglossians, Calomiris and Haber demonstrate that bargains change with the underlying social forces—sometimes even for the better.

In the authors’ accessible form of game theory, wealthy elites need to park their cash and obtain loans for their enterprises. The state’s executive needs bond buyers to finance wars. The larger public wants to borrow cheaply for current consumption. Each has an incentive to weaken (and for the executive, to expropriate) the others. Madison anticipated these incentives in Federalist 10:

Recommended Stories

This struggle plays out across the centuries. The 2008 collapse turned grand theoretical economic models like Keynesianism, monetarism, and rational expectations into gods that failed, and the focus shifted to comparative institutional histories. The authors’ prodigious research across countries and time recalls Carmen Reinhart and Kenneth Rogoff’s This Time Is Different: Eight Centuries of Financial Folly (2009), although Calomiris and Haber believe that political systems, rather than debt, are the problem.

The Bank of England, created in the wake of the Glorious Revolution of 1688, is usually apotheosized as the first modern central bank. Here, it represents an oligarchic coup against absolute monarchy: Commercial banks within the charmed circle received support while country banks outside it often failed. Industrial Revolution entrepreneurs were forced to self-finance, slowing their expansion and delaying the industrial takeoff.

The authors exaggerate the banking clique’s power: King William III—whom the Glorious Revolution brought to power, thus launching the second Hundred Years’ War with France (1689-1815)—wanted war funding even more than the oligarchs did, and he happily traded residual absolutist claims for cash. The bank, facing gigantic financing strains, became a serial defaulter on gold payments over the course of the long war. Struggling to fulfill its primary war finance mission, it had little desire to fund high-risk, high-tech Industrial Revolution startups. Calomiris and Haber argue that the credit system opened up in the wake of pressure created by the national mobilization for the French revolutionary wars, but they downplay the post-Napoleonic peace dividend, which gave the Bank of England the flexibility to protect a broader public in credit crises.

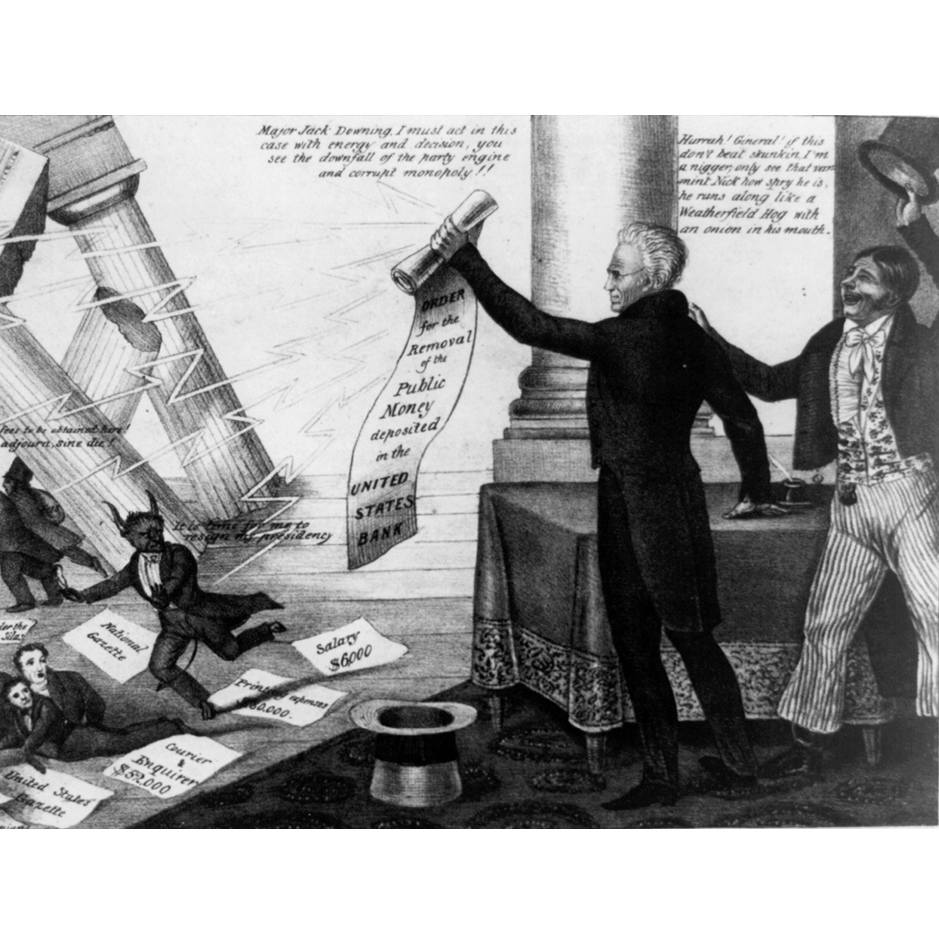

In decentralized America, local elites played on populist sentiments to promote easy money—and resist competition from money center banks. In a 30-year national career, Madison was against a central bank before he was for it—before he was against it, before he was for it. The Father of the Constitution also fathered a quarter-millennium of credit bubbles, inconsistent regulation, and banking collapses. The party really got underway when Andrew Jackson fueled a giant land, cotton, and slave bubble by destroying the Second Bank of the United States (the era’s central bank) and then triggered a global depression by suddenly demanding federal land payments in gold or silver.

Later generations also pursued populist-sounding regulations that entrenched and bailed out local elites. Far from stabilizing the financial system, the Federal Reserve, as created in 1913, limited the power of the relatively responsible New York banks over nonmoney center banks. Early 20th-century state branch banking restrictions and deposit insurance funds prevented larger banks from competing with local banks on the basis of safety. When local banks failed in the Great Depression, the same interests created the Federal Deposit Insurance Corporation (over Franklin Roosevelt’s fierce resistance) to put the federal taxpayer on the hook towards the same end.

This tale of a federalist fig leaf for local rent-seeking underplays the difficulty of managing the 19th-century American banking system. With an economy heavily dependent on agricultural exports and rapid territorial expansion from the Appalachians to the West Coast, the United States needed huge amounts of European (mainly British) credit from the time of the end of the Napoleonic Wars through the Great Depression. Long-term credit for the construction of canals and railroads required predicting revenues from land to be incorporated into international markets. The annual agricultural cycle required gigantic short-term credit (funding crop planting and agricultural equipment) flowing from European lenders to American money center banks, then to local banks in chronically cash-short agricultural regions. Payment would come as much as a year later, following delivery of the harvest to European markets, only to be rolled over into new annual loans.

The difficulty of assessing credit over such long distances and so much time made crashes and failures almost inevitable. Canada, the authors’ banking paragon, became a major agricultural exporter only in the last third of the 19th century, when telegraphs, railroads, steamships, and futures markets collapsed transportation times and information costs. In Brazil, with minimal rule of law and a closed oligarchy, the picture was still grimmer: Elite-controlled banks dominated the financial sector, steering cheap credit and bailouts to affiliated enterprises, starving the central government, and choking off competition from other sectors in the society. The 19th-century Mexican dictator Porfirio Díaz created a stable banking system that funded elite enterprises in exchange for near-absolute political power and a market for his government bonds.

Unlike the English and American systems, which were constrained by dispersed power and political continuity, regimes in closed societies faced endgame problems. Threatened elites would loot the financial system through bond defaults, hyperinflation, bank insolvencies, or confiscations. Vladimir Putin provides a ripped-from-the-headlines example: When the massive dollar-denominated debt of energy company Rosneft became unserviceable in the wake of the ruble crash, the Russian central bank accepted Rosneft bonds held by commercial banks as loan collateral, effectively converting roughly $10.8 billion of crony debt into government obligations and injecting a potentially inflationary 625 billion rubles into the economy.

In the 20th century, as voting rights expanded, so did populist regimes—often in previously oligarch-controlled countries, such as Brazil. Governments assuaged lower-income groups with lavish welfare states, financed by requiring banks to buy their bonds, then effectively wiping out consumer bank accounts through inflation and devaluation (as in Venezuela) or confiscation (as with Argentine pensions). While military rule led to banking stability in Augusto Pinochet’s Chile, a Brazilian junta accelerated its populist predecessors’ banking destruction.

Scotland and Canada are among the few bright spots here. Both developed oligopolistic branch banking systems that spread deposits and loans nationwide, maintained a modicum of competition, diversified risk, and provided widespread credit without collapses. While analyzing the internal bargains that made this possible, the authors neglect the external limits on elite depredations: Scotland and Canada shared a Calvinist culture of thrift and rectitude; even after massive immigration, Canada remains, culturally and ethnically, part of Greater Scotland.

Even more important, these two thinly populated countries existed at the sufferance of the British economic giant—and in Canada’s case, of the United States as well. Imprudent elites risked being subsumed: The financial crisis following the failed Darien colonial scheme had already ended Scotland’s political independence in the Act of Union (1707); during the Great Depression, Newfoundland’s financial collapse led to a British takeover, then forced incorporation into Canada.

The biting final chapter offers a précis of the banking games that political systems play, serially demolishing the leading economic and political nostrums for banking stability. Calomiris and Haber offer a soupçon of hope: When crises upend political constellations, new coalitions may defeat rent-seeking interests and create stabler systems that benefit society. They allow themselves to hope that the United States may be in such a moment. The Community Reinvestment Act, which forced banks to make bad housing loans to low-income borrowers in exchange for permission to merge, contributed to the housing meltdown—and created a set of oligopolistic nationwide banks with the potential to push back against reckless lending practices.

Yet even this may be too sanguine. The oligopolistic banks were relatively prudent during the bubble, so shadow banking and government guarantees filled the gap. The Obama administration is trying to restart reckless lending through a combination of looser standards for government guarantees and extortionate litigation against banks for ill-defined offenses. With risk socialized, the big banks have little incentive to challenge the housing populists running the government.

Margaret Thatcher maintained that “there’s no such thing as society,” just people pursuing their interests. Calomiris and Haber suggest that there is no such thing as “the banking system,” just rent-seeking interests trying to manipulate institutions for their own ends. Whereas Baroness Thatcher also exhorted people to look after their neighbors, Fragile by Design is a call to action for people to seize the moment to resist crony capitalism.

Jay Weiser is associate professor of law and real estate at Baruch College.