When the Trump administration unveiled its 2020 budget proposal this week, attention quickly focused on its strong assumptions about future economic growth. The budget assumes 3 percent average GDP growth across the next decade, with 2019 hitting 3.2 percent, a bit stronger than 2018’s 3.1 percent. From there, the number tapers back down to 3.1 percent in 2020, and finally locks in at 2.8 percent by 2026.

These numbers ride higher than those of most private forecasters, as well as those of the Congressional Budget Office, which assumes growth will average close to or less than 2.0 percent.

How likely are we to realize the administration’s optimistic forecast?

To address the question, we must examine two, and only two, pieces of information. Ultimately, the limits of GDP growth are set jointly by these two economics forces. They are the number of people who go to work each day, and how productive those workers are.

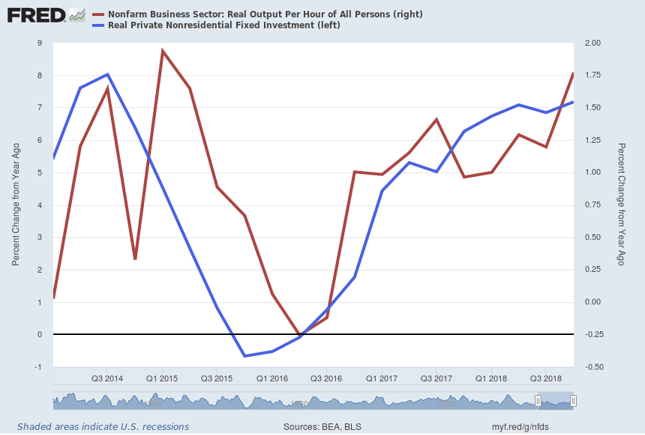

An examination of just-arrived data for 2018’s fourth quarter suggests the administration may be on the side of the data angels, or vice versa, at least for now. The next chart shows that year-over-year growth in output per hour for U.S. labor, labor productivity, in other words, hit 1.76 percent.

The chart contains another piece of data that explains why. Growth in private sector capital investment tends to foretell improvements in labor productivity. Our newly lowered income taxes, which are not shown, help explain why capital investment would be growing.

Is that enough to ensure 3.2 percent GDP growth this year? The 1.76 percent growth in productivity means we would need to see at least 1.44 percent growth in the size of the labor force. Once again, the data angels sing. The U.S. labor force grew by 1.46 percent in 2018’s fourth quarter on a year-over-year basis.

Put another way, current data on the U.S. economy tell us that the economy’s speed limit is hitting 3.2 percent. But, as the poets say, it takes more than one robin to signify that spring has arrived. The remaining question is whether or not we can stay on pace.

Kevin Hassett, chairman of the Council of Economic Advisors, indicates that the 2020 budget plan assumes that the 2017 changes in corporate taxes will be extended, which would continue to drive stronger corporate profits and larger capital investments. That, as we’ve learned, can lead to continued growth in labor productivity.

As for labor force growth, Hassett points to rising levels of labor force participation as an indication that even in times of low population growth, we can still enjoy the contributions of a growing labor force.

But to experience this happy outcome for a decade, we need a bit of cooperation from Washington politicians. Here’s a handy checklist: Elimination of all currently imposed tariffs and declare peace on the trade-war front; no more government shutdowns; no more tax increases; and no more de novo regulatory initiatives.

Is this too much to hope for? Unfortunately, I believe it is. But I sure like thinking about it.

Bruce Yandle is a distinguished adjunct fellow with the Mercatus Center at George Mason University and dean emeritus of the Clemson University College of Business and Behavioral Science. He’s the author of the new policy brief, “The Economic Situation, March 2019.”