In spring 2015, 18 months before the 2016 elections, the tax reform legislation of 2017 was taking shape. Virtually every Republican candidate was talking about fixing the broken tax code with pro-growth tax reforms which reduced tax rates and broadened the base. After winning the White House and maintaining control of the House and the Senate, Republicans enacted their tax reform plan within their first year.

Now, in spring 2019, 18 months before the 2020 elections, the tax increase bill of 2021 is taking shape.

Recommended Stories

Virtually every Democratic presidential candidate is talking about undoing the 2017 tax reform and raising taxes on the wealthy and corporations, and a long list of specific tax increases is under serious consideration.

As a result, the largest tax increase ever enacted could happen if the Democrats win the White House, retain the House, and regain control of the Senate.

Every taxpayer should start preparing now for the possibility of these tax increases, and more importantly, begin making the case for how damaging these tax increases would be to the economy, our financial markets, and economic prosperity.

The following is a brief summary of the actual tax increases proposed by Democratic presidential candidates and members of the House and Senate, and which will be ready for enactment in 2021.

Individual Taxes: Congressional Democrats (Reps. Rosa DeLauro of Connecticut, Jan Schakowsky of Illinois, and others) have proposed a repeal of the individual tax cuts enacted in 2017, a massive tax increase for millions of middle-class taxpayers, a return to a top tax rate of 39.6%, and a 5% surtax on top of that. Several House members (Reps. Alexandria Ocasio-Cortez of New York, Ayanna Pressley of Massachusetts) have called for a 70% top rate, while another one (Rep. Ilhan Omar of Minnesota) wants a top rate of 90%. Other members have proposed sharply higher payroll taxes to fund new government spending programs.

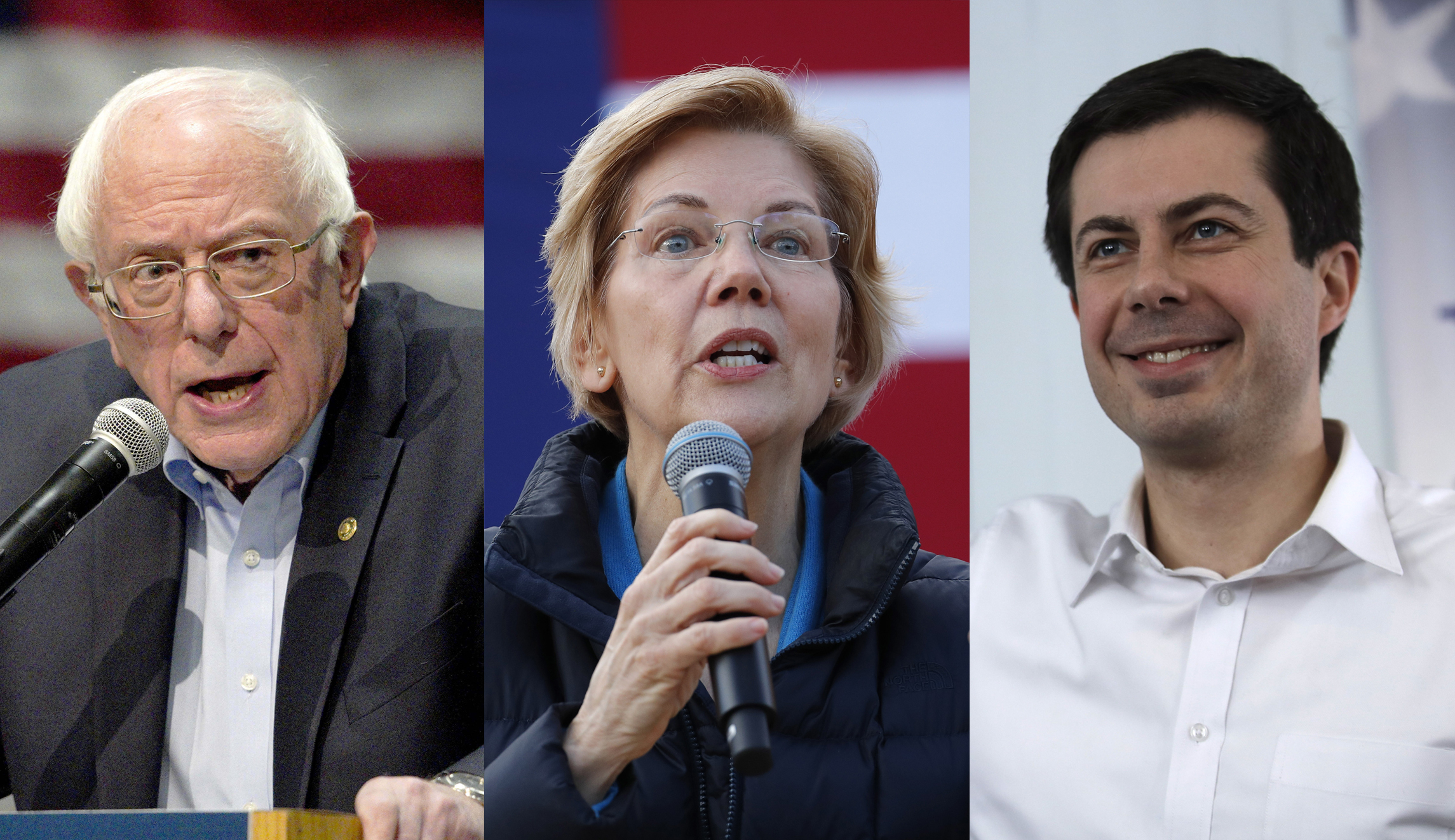

As if this is not enough, a number of presidential candidates (Sen. Elizabeth Warren of Massachusetts, South Bend, Ind., Mayor Pete Buttigieg, Sen. Bernie Sanders, I-Vt.) have proposed a new wealth tax, to be levied every year on some Americans’ assets and property. Once in place, it will almost certainly be expanded every year to cover more people.

Corporate Taxes: Many Democrats want to repeal the corporate tax reductions enacted in 2017, raising the corporate tax rate back to 35%, close to the highest rate in the world. Others are pushing for raising the 21% rate to 28%. One candidate (Elizabeth Warren) wants to go even further, imposing a new 7% tax on corporate profits above $100 million, a tax that would hit 1,200 businesses and surely result in job losses and price increases.

Investment Taxes: In addition to raising the top individual and corporate tax rates, which would reduce saving and investment, many legislators and candidates also want to tax capital gains as ordinary income, raising the maximum rate to more than 40%. Sen. Ron Wyden, D-Ore., has gone even further, proposing to tax, at the new higher rate, unrealized capital gains annually, rather than when sold. Wyden and many others also want to tax capital gains at death.

In addition to taxing capital gains, numerous candidates (Sens. Kirsten Gillibrand of New York, Bernie Sanders, Elizabeth Warren) and House and Senate members (Rep. Peter DeFazio of Oregon and Sen. Brian Schatz of Hawaii) want to impose a tax on stock and bond transactions. This financial transaction tax would hit workers’ pension plans and the retirement savings of millions of middle-class families.

Estate Taxes: A number of proposals have been advanced to raise estate taxes. One proposal from Sanders would reduce the estate tax exemption from $11 million to $3.5 million, which would hit family farms and small businesses, and raise the top estate tax rate to 77%.

Tax increase proponents say these tax increases will only hit the wealthy and big corporations, claims which resonate with many voters. But to raise the revenue needed to pay for the many new promised spending programs, the actual tax increases will need to be broad based and hit every taxpayer in the country.

Over the next 18 months, voters need to hear how these tax increases will damage the economy and their economic future and well being. These tax increases will reduce take-home pay, destroy millions of jobs, harm financial markets, and reduce the saving and investment needed to keep the economy growing. If these tax increases are enacted, our roaring economy, with higher than 3% growth and the lowest unemployment rate in 50 years, will come to a crashing halt.

Bruce Thompson is a contributor to the Washington Examiner’s Beltway Confidential blog. He is a consultant in Washington. During the Reagan administration, he was Assistant Secretary of the Treasury for Legislative Affairs.