Until very recently, the economy was spinning its wheels — or, as readers of this column might remember me saying, “sleepwalking.” Couched in terms of real GDP growth, the nation was slogging along at less than 2 percent growth in 2016 and then at a pale 2.2 percent in 2017 — 3.2 percent is the long-running average, if we go back to the 1950s when calculating.

But then in the latter part of 2017, something happened. The sleepwalking economy seemed to awaken, rub its eyes, and begin to trot. Growth accelerated.

The second quarter growth in 2018 came in at 4.2 percent and third quarter growth at 3.5 percent. Whether because of tax cuts, deregulation, higher consumer confidence, or the sudden surge of animal spirits, the economy stirred.

At least until now. Instead of continuing to grow at a high pace, it currently seems to be hesitating. The Dow Jones closed 800 points (3.1 percent) lower on Tuesday. Year-to-date growth in the three major indices has been weak.

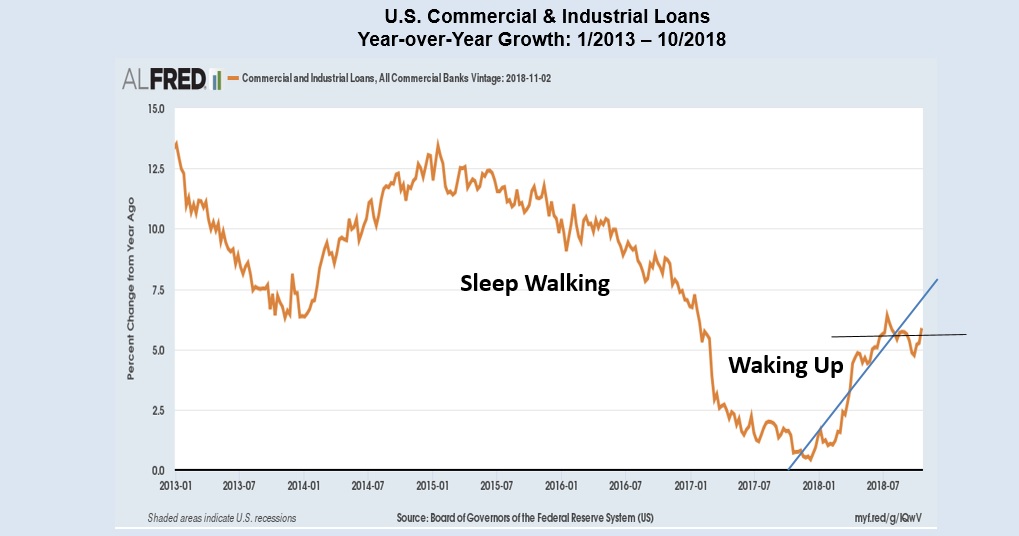

Take the accompanying chart, which clearly shows the progression from sleepwalking to waking up to hesitating, as one example. Using Federal Reserve data from January 2013 to October 2018, it reports year-over-year growth of commercial and industrial loans for the U.S. banking system. Notice how the growth rate peaked around January 2015 and then slowed until January 2018. After January 2018, lending accelerated until around July this year, when the growth rate plateaued and now hesitates.

An examination of employment growth for the economy reveals a somewhat similar sleepwalking and waking up phase that follows the lending pattern. But the employment data show no hesitation thus far. Employment growth is still bouncing around a positive trend. Probing a bit deeper, part of the positive employment picture can be explained by higher growth in temporary worker hiring — which is, unfortunately, another sign of economic hesitation.

What’s going on here? Why the hesitation? And will it go away?

There are a host of factors that go into the recipe for our economy’s performance. Fundamentally, economic growth can only go as far as the combination of labor force growth and labor productivity growth can take it. Both of these numbers are rather weak, and are not likely to take a sudden surge.

This said, it is fair to suggest that two other factors (which readers of this column know all too well) are particularly relevant when considering bank lending and employment: Fed interest rate policy and White House trade policy.

Just recently, Fed chair Jerome Powell revealed a somewhat relaxed position on interest rate hikes, and President Trump has announced a truce of sorts regarding trade wars with China. Maybe these two actions will be enough to re-accelerate growth. If so, what we are seeing now may later be labeled the policy pause that refreshed the economy.

Let’s hope the pause on tariffs and interest rate uncertainty lasts more than 90 days, and the acceleration that ensues takes us back to stronger growth.

Bruce Yandle is a contributor to the Washington Examiner’s Beltway Confidential blog. He is a distinguished adjunct fellow with the Mercatus Center at George Mason University and dean emeritus of the Clemson University College of Business & Behavioral Science. He developed the “Bootleggers and Baptists” political model.