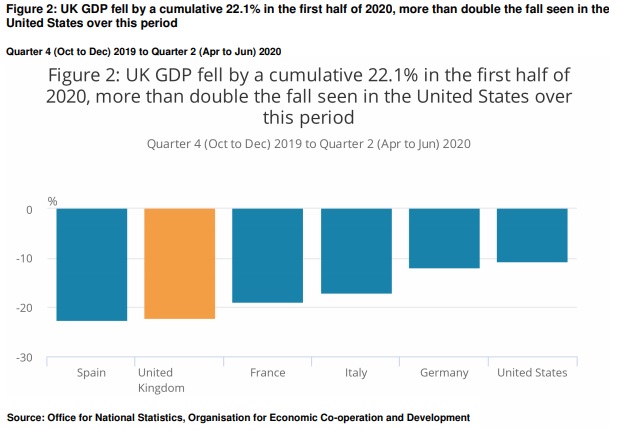

Contrary to what you might have been told, a 32.9% fall in GDP is a smaller decline than a 22.1% one, or even an 11.9% decline. Those are the economic slowdown estimates for, respectively, the United States, the United Kingdom, and Germany. It’s not magic, or deceit, or even American exceptionalism that explains why that 32.9% is actually smaller than 22.1% and 11.9. It’s because the U.S. reports economic changes on an annualized basis (meaning it shows how bad it would be if the quarter continued all year), while everyone else just lists what happened during those three months. Removing that trick means that the U.K. saw a 22.1% economic decline in the second quarter, Germany saw an 11.9% decline, and the U.S. economy contracted by “only” 10.6%. You can see it all clearly in the below graph.

Yes, yes, of course, it’s election time and “Orange man bad!” and all that, but actually, the American response to the economic troubles has been pretty good — better than other major economies.

As to why it has been better, one clear and obvious reason has been the speed at which things have been done in the U.S. It’s possible that $600 bonus on unemployment benefits was a bit excessive or that stimulus checks weren’t really necessary, but what was done was done quickly. That paragon of social democracy, the European Union, is only just done arguing about who is going to pay for it all — much of the money won’t even be spent until next year.

In recessions, as with so much of the real world, there are times when immediate action is crucial. Even imperfect action is better than just discussing action. Our standard economics here tells us that in such a recession, to stop it becoming a depression, we need to get the money out the door right now. The U.S. did that well. Alternative plans may have done 5% or 10% better, but the important thing is that action was taken quickly.

This is why the American economy is roaring back. Unemployment has been falling by significant fractions of a percentage point each week. By the scales of such things, this is huge. Retail sales are higher than they were a year ago. Durables (an indication of both investment and confidence in the future) were up 11% just this last month. We could even point out that the level of U.S. unemployment, now at little under 10% in the aftermath of the terrible coronavirus recession, is about the same figure as France has in normal times — ah, the joys of socialism.

Of course, I’m not trying to say that everything is peachy — it isn’t. It’s also not true that President Trump is solely responsible for everything that’s gone right. But the U.S. economic reaction to policy about the coronavirus has done rather well, better than most other places. Guess whose desk that buck stops upon?

I expect the U.S. economy to continue to recover better than nearly all other places, simply because it is a more flexible economy to start with. All those things frequently decried such as job insecurity, fire at will, and the lack of worker job protections are exactly what make it possible to adapt to the vicious economic changes we’ve recently had and come back stronger. Those are largely baked into the system and aren’t the result of the Trump administration, but it would be a pity to elect the people determined to destroy that very flexibility just as that flexibility has proven its usefulness.

Could things have been done better at points? Sure, and hindsight is 20/20 too. But the overall economic performance of the U.S. has been pretty good these past months compared to what other countries achieved under the same pressures. You have to give America, and the guy running the country, some credit for that.

Tim Worstall (@worstall) is a contributor to the Washington Examiner’s Beltway Confidential blog. He is a senior fellow at the Adam Smith Institute. You can read all his pieces at The Continental Telegraph.