Since 1970, there have been six U.S. recessions. All but two were associated with a collapse of mortgage lending, and therefore housing construction, following Federal Reserve actions that raised interest rates. These are casually called “credit crunches.” The other two, in 2001 and 2007-2009, were different. The 2001 recession was associated with Sept. 11, and the Great Recession was associated with the sub-prime mortgage debacle.

We now face the possibility of another housing slowdown and related recession. This one might again fall into that “different” category.

Instead of being caused by a Fed run-up in interest rates, terrorist attack, or credit market collapse, the danger of a new housing crunch comes from Trump administration tariff policies. Targeted tariffs on lumber, steel, and aluminum — building materials, in other words — are now beginning to form a cost wedge that could close off the nation’s housing construction boom.

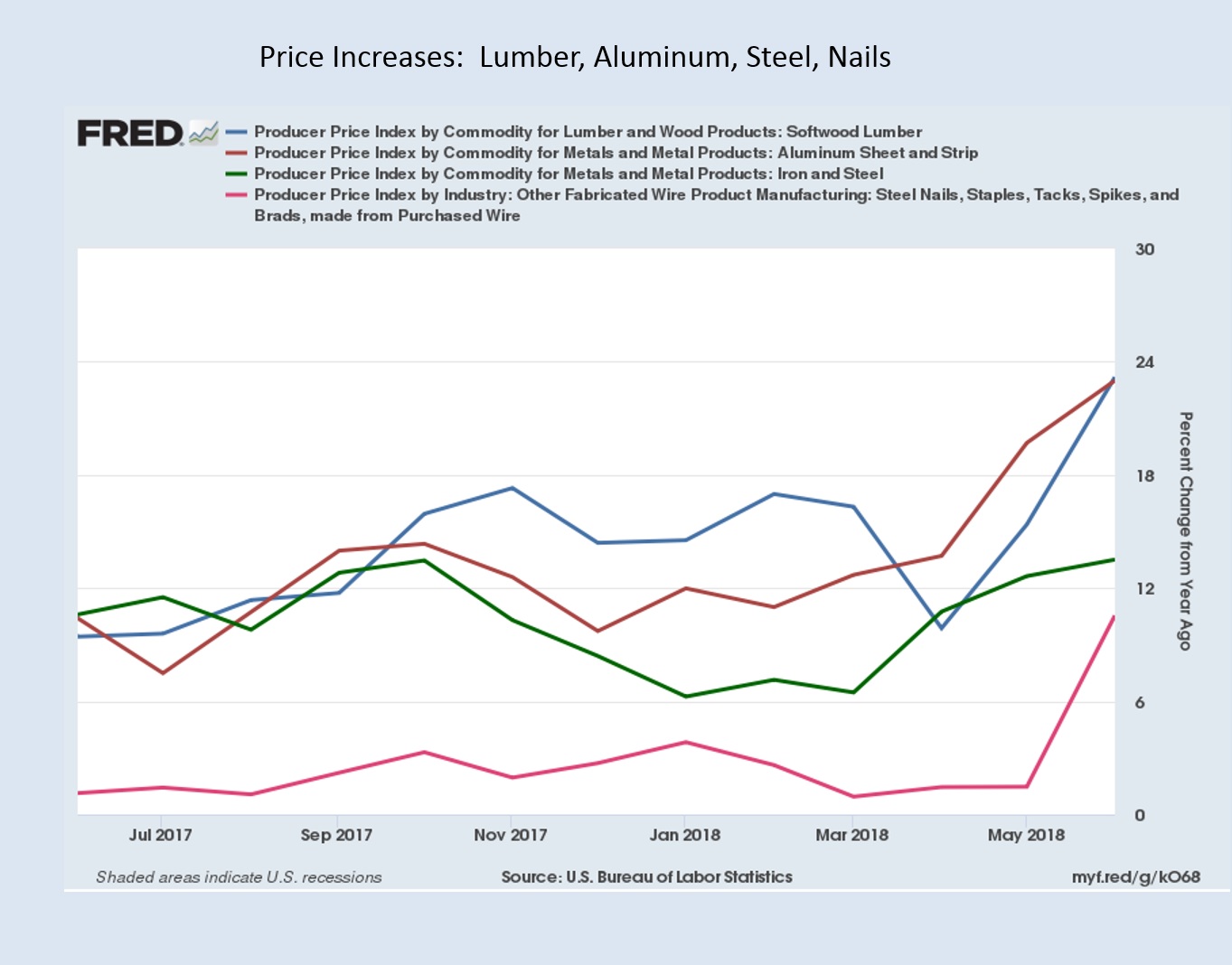

Using data and chart-making capabilities provided by the Federal Reserve Bank of St. Louis, I have mapped year-over-year changes in producer price indexes, or PPIs, for softwood lumber, steel, aluminum, and nails and other steel-wire products. Each is subject to one form or another of Trump administration tariffs. The timing of the tariffs is apparent in the chart, a trend line suddenly bends upward.

[Also read: Layoffs from Trump’s tariffs may overtake job gains from tax cuts]

As also shown in the accompanying chart, the price index for softwood lumber and aluminum increased almost 24 percent in June 2018 relative to a year ago. The iron and steel PPI, which includes rebar, was up almost 14 percent for the same period. Nails and other steel-wire products jumped more than 10 percent.

And what about housing? Permits for the construction of privately owned housing units fell in April, May, and June of this year. Housing construction data for newly permitted units generally follows about 60 days later. Housing construction fell significantly in June, the most recent month for which we have national data. We must now wait to see if the trend continues.

And then there’s the Fed.

The Federal Reserve Open Market Committee assures us that more interest rate increases are on the way. And current data on inflation and tight labor markets suggest the Fed can offer a traditional explanation for hitting the interest rate brakes. But when that happens, the interest rate run up will join forces with the substantial tariff-induced building material cost increases that already appear ready to take a bite out of new home construction.

If this scenario comes to pass, the burden of putting America “first” on trade once again falls on the shoulders of Americans. This time it’s U.S. home buyers.

Bruce Yandle is a contributor to the Washington Examiner’s Beltway Confidential blog. He is a distinguished adjunct fellow with the Mercatus Center at George Mason University and dean emeritus of the Clemson University College of Business & Behavioral Science. He developed the “Bootleggers and Baptists” political model.