When the Department of Commerce announced on Thursday that the advanced estimate for second-quarter GDP growth came in with a bone-chilling 32.9% decline on an annualized basis, Congress was debating the details of another multitrillion-dollar relief package for America’s beleaguered, coronavirus-fatigued population. An extended federal supplement for the more than 20 million unemployed people, along with perhaps another round of cash payments for families, will almost surely be finalized before Congress goes on recess.

But while our legislators deliberate and the coronavirus surges, GDP growth (which until the pandemic was weak but improving) seems to be caught in a downdraft. Another shipment of money from Washington may help us weather the storm, but GDP growth will continue to disappoint unless the money actually gets spent.

Recommended Stories

The latest report on coincident economic indicators from the Federal Reserve Bank of Philadelphia helps to put some dimension on how things looked through June across the 50 states. The June estimate indicates that economic conditions improved in 42 states. This was up comfortably from the May estimate, when 34 states showed improving conditions, and up a huge amount from April’s numbers when not one single state showed improvement. To put it mildly, the data showed a happy, positive trend.

But this was before the July coronavirus surge across the Sun Belt and other areas brought increasing levels of infection. Common sense and state actions taken to retighten crowd-limiting rules tell us that virus hot spots bring diminished economic activity. Thus, the happier trend observed in the June data seems to be running out of gas.

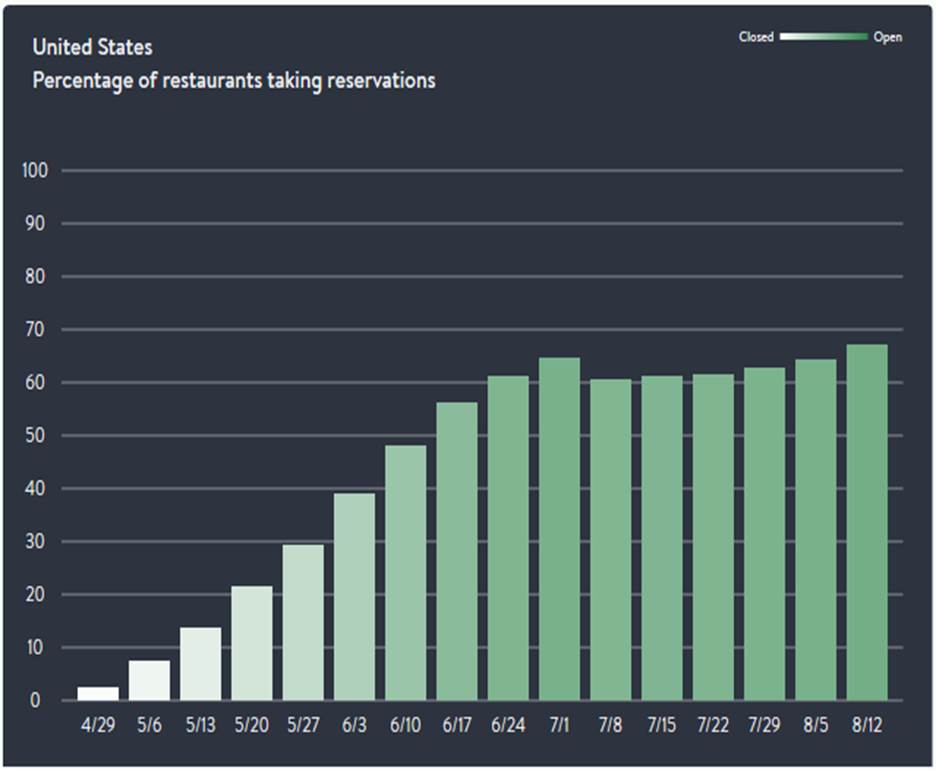

Glimmers of weakness are seen in the Conference Board Consumer Confidence Index, which fell to 92.6 in July after having risen to 98.3 in June. A practical picture of what happens when people are frightened and restaurants are shut down comes from OpenTable in the below chart, which shows the percentage of restaurants taking reservations.

Notice how the bars stop growing after July 1. (Not all the data are discouraging, however — the American Staffing Association’s weekly index measuring growth in temporary and contract employment rose to 69.7 for the week ending July 19, after having been as low as 59.9 for the week of May 10.)

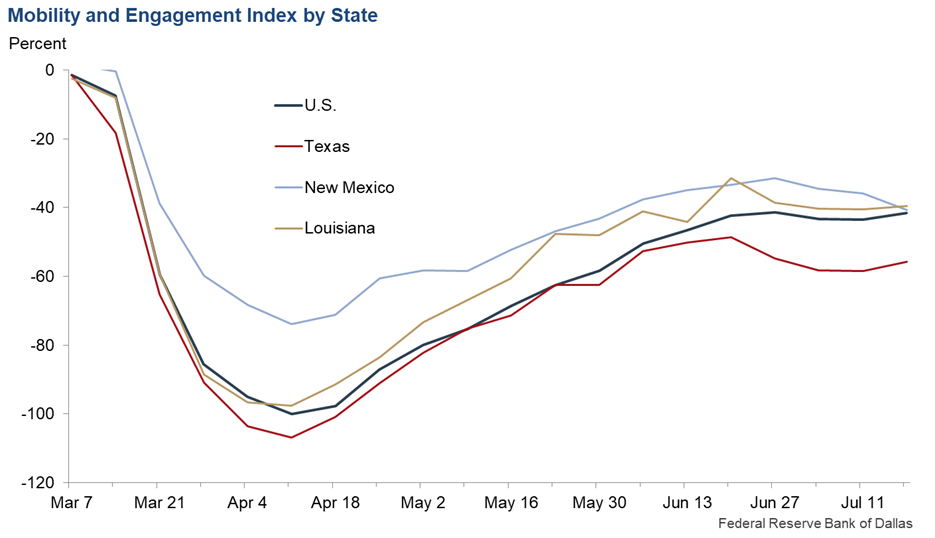

An even more persuasive picture of a stalled economy is seen in a newly created index of mobility and engagement developed by the Federal Reserve Bank of Dallas. Shown in the next chart, the Dallas Fed index is based on population movement traced by cellphone technology (without, I should add quickly, compromising individual privacy, or so it is claimed).

The data provide evidence on the extent to which people are venturing away from home and staying longer when they do so. As the chart indicates by the U.S. line, mobility that was increasing through June 27 is now stagnant. We get a somewhat similar reading for the three states contained in the Dallas Fed’s district.

So, what does all this say about GDP growth prospects and efforts by Congress to bring balm to the economy? First off, balm is always welcomed, but if there’s another round of cash payments, don’t expect them to give new energy to our flagging economy. So far, much of the stimulus cash income has gone into individuals’ savings. There is fear out there and also few places to shop. This set of conditions is set to continue until some of the coronavirus surge is capped. In spite of this, the economy is still reknitting its badly torn structure. Yes, manufacturing is recovering somewhat, construction is surging, and the services economy is chugging.

The worst part of the coronavirus recession lies behind us. Better days lie ahead, but movement to happier times will be slow.

Bruce Yandle is a contributor to the Washington Examiner’s Beltway Confidential blog. He is a distinguished adjunct fellow with the Mercatus Center at George Mason University and dean emeritus of the Clemson University College of Business & Behavioral Science. He developed the “Bootleggers and Baptists” political model.