Last Friday’s Census Bureau report on July retail sales for the nation brought a welcome dose of good news, but it also underlined some concerns for the future.

Starting with the good news, sales for July rose above June’s tally by 1.2%. But that was just part of it. Of greater importance, perhaps, is that July 2020’s sales exceeded the July 2019 level by 2.7%. Many people would be very surprised to learn that sales activity is better now than it was a year ago.

In a word, it’s a good time to take off our coronavirus worry hats for a day or two and celebrate. But if we do, the celebration should be brief.

Data in the Friday report and elsewhere indicate that the pace of recovery, while positive, is weakening, and for one simple reason: Too many businesses are still closed. No matter how much money Congress ships to people, the speed with which the economy reopens will determine future gains in retail sales, as well as economic growth generally. If too many stores and restaurants remain closed (or must close again), a lot of the money will stay in savings.

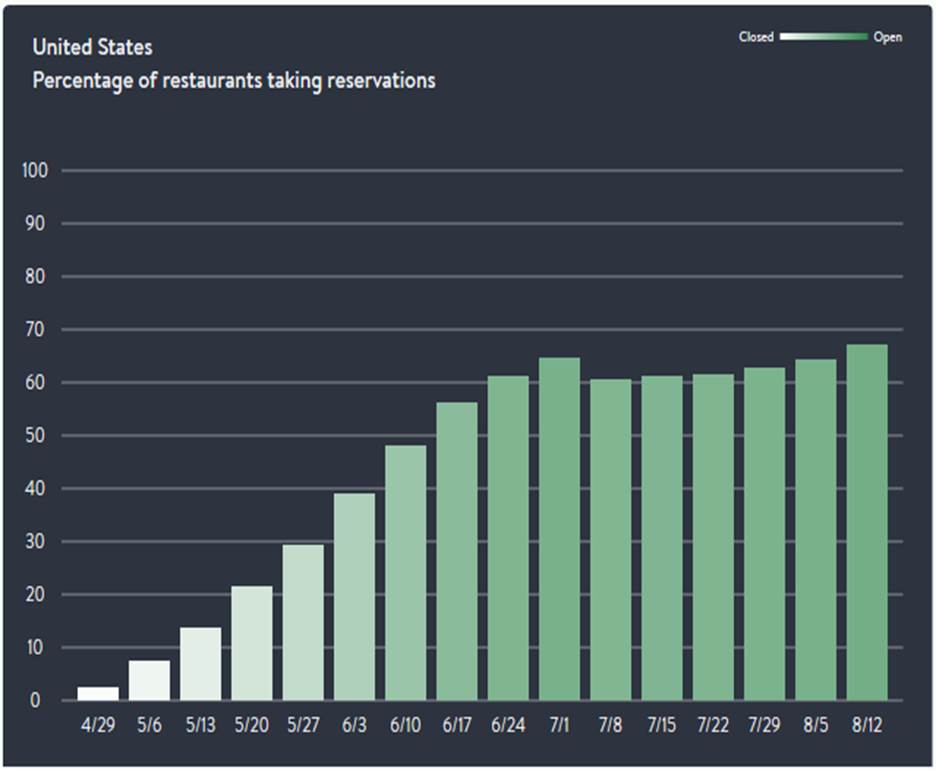

Consider once again OpenTable’s data showing the percentage of U.S. restaurants that are open and taking reservations. I have written on this important data before, since it is a proxy for the extent to which the full economy is open. Here, you can indirectly see the prospective weakness in retail sales and economic growth reflected.

In the above chart, I report the data for late April through Friday. Notice how openings accelerated across May and June. Then, look at the flattening of the curve that followed. We can also see weakness showing around July 8, when some states that had opened up cut back. We now have a plateau. This particular curve has flattened just when we would like to see it rising.

The July retail sales data also tell us about economic sectors that are doing well, as opposed to some that are still struggling. Large July sales increases are seen in food and beverage stores, building and garden supplies, sporting goods, hobby, musical instruments, and books. Significant weaknesses are found in clothing and clothing accessories and gasoline stations.

But while the data tell us that people are buying groceries and apparently doing a lot of home cooking, the sales growth generated for that category, a monthly gain of 11.1%, is not nearly large enough to offset the 12.9% loss in restaurant and drinking place sales. And this is where another rub comes.

Employment in restaurants and bars was, as we know, hit especially hard by coronavirus limitations that shut down parts of the economy. According to the Bureau of Labor Statistics, there were 12.0 million employed in this sector in July 2019. In July 2020, a year later and even after some improvement from the month before, the number was down to 9.2 million.

A glance back at OpenTable shows how closely that data parallels what has happened with employment numbers. The 12-month loss in jobs is about the same as the shrinkage in restaurants taking reservations.

Yes, retail sales, a critically important indicator of economic activity, are looking good, but the prospects for further acceleration depend on the same major economic factors that so much else still depends on. More masks, more social distancing, more testing, and ultimately a reliable vaccine may generate a more confident economy.

We must wait and see. Meanwhile, we must count on our neighbors and their collective common sense to sort things out as best they can.

Bruce Yandle is a contributor to the Washington Examiner’s Beltway Confidential blog. He is a distinguished adjunct fellow with the Mercatus Center at George Mason University and dean emeritus of the Clemson University College of Business & Behavioral Science. He developed the “Bootleggers and Baptists” political model.