It’s time for a look at some of the good and the bad in the economy. Let’s get the bad out of the way first.

In recent days, we have been hit with multiple bad news readings on the economy. For example, the Institute for Supply Management November index for manufacturing arrived at a low 48.3, the fourth month in a row with readings less than 50, which means that the production side of the economy is contracting.

But we must remember that Boeing is still wrestling with its grounded 737 MAX problem and that General Motors has just ended a production-crippling strike. Even so, a few days later, the ISM’s index for the services economy, what may be thought of as the rest of the economy, came in with a lower-than-expected reading of 53.9. While still showing an expansion, the index has followed a rather jagged decline since December 2018 when it stood at 58.0.

To top it all off, the Atlanta Fed’s Dec. 2 running estimate for fourth-quarter GDP growth arrived with a chilling 1.3% reading. If this number were to become final, GDP growth for the year would barely break 2% after a much-healthier 3.1% in the first quarter.

Now, all this ISM and GDP business may be important, but what about the really important stuff?

Like jobs. With good news on job growth for November, the unemployment rate is still in record-low territory, and year-over-year growth in employment is getting stronger. But, after clawing around in the jobs data, one finds that in October, the hiring pace for temporary workers turned negative for the first time since December 2016. This is bad news for permanent payroll workers if it continues.

We all know which sectors are showing the most pain. Really, you could call it one sector: manufacturing and exporting industries within manufacturing. Yes, President Trump’s expanding trade wars may ultimately lead to something positive for all Americans taken together, but right now, the tally doesn’t look too good.

Well, isn’t there any good news out there? As President Reagan famously said, “There must be a pony in here somewhere.” And there is.

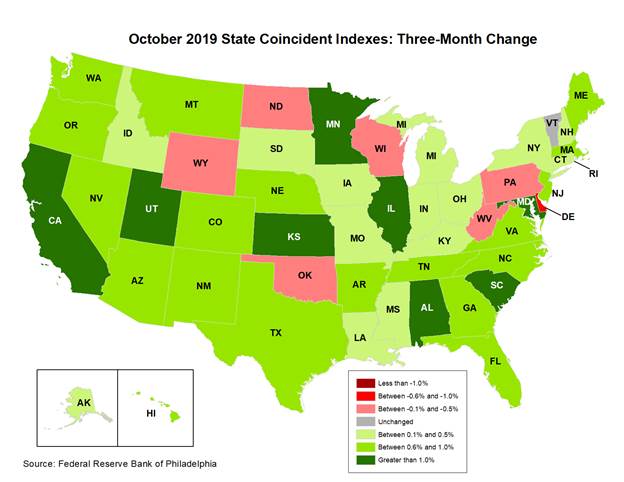

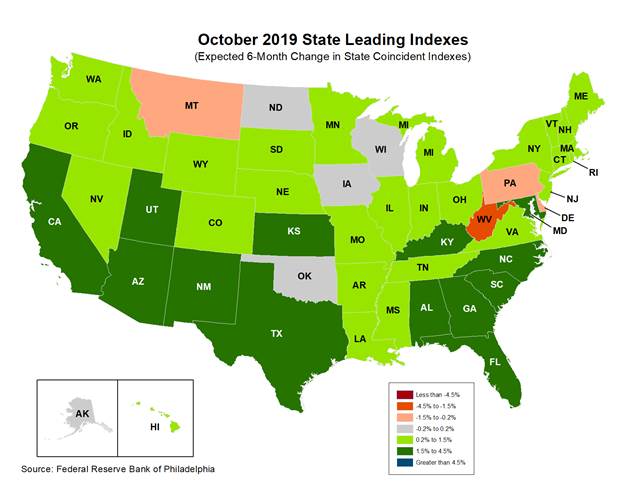

The good news pony is hiding in the Philadelphia Fed’s most recent estimates for current and future state economic activity. In the past, you may have read about how these estimates can help to gauge the effects of our trade policy or the well being of key political constituencies. Here, I show 50-state maps for October state coincident indicators — how state economies are doing right now — and for state leading indicators, which look six months out.

A comparison of the future outlook with the present should bring a smile. Around April, things look much better than they do currently, with pink states turning gray and green.

So what does the combination of bad news/good news tell us?

First off, the data suggest that as the year ends, things are definitely slowing. The short-run trend will likely continue for some parts of the economy, especially for the manufacturing export side. But the good news reading tells us there is probably no recession lurking in the woods, at least for the year ahead. Put this together, and we get a GDP growth reading of around 2% or a bit less for the year 2020.

Yes, even with Thanksgiving over, we still have more to be thankful for.

Bruce Yandle is a distinguished adjunct fellow with the Mercatus Center at George Mason University and dean emeritus of the Clemson University College of Business and Behavioral Science.