As Congress looks for solutions to solve the looming Social Security crisis, a gradual increase in the retirement age should be a top priority.

When Social Security first began in 1935, it was meant to provide security for the elderly. Now, almost 80 years later, demographics have changed and “elderly” has taken on an entirely new meaning.

A 65-year-old in 1930 could expect to live to age 77. Today’s 65-year-olds can expect to live until age 84. That’s seven additional years of collecting Social Security benefits. Yet the Social Security retirement age has risen only one year in that span.

The premise of Social Security was that the working population would pay benefits for the elderly population. A nice funding mechanism in theory, but the elderly population has been growing and collecting more benefits.

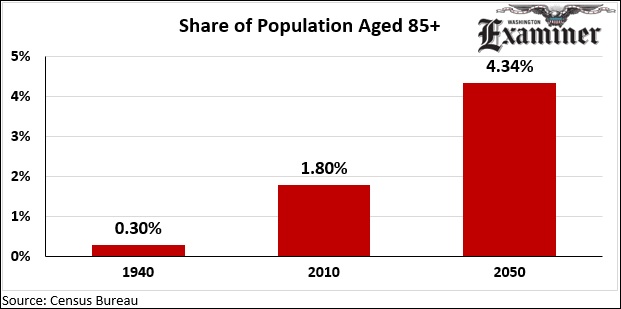

In terms of percentage points, the 85-years-and-older population will grow more in the next 40 years than it did in the last 70 years. In 1940, just 0.3 percent of the population was 85 years old or higher. Seventy years later, that figure is 1.5 percentage points higher. In the next 40 years, it will rise another 2.5 percentage points. If you think Social Security is expensive now, just wait until the share of Americans who receive benefits for at least 20 years doubles.

Quality of life is much better for a 65 year old today than it was in 1935. The working environment is also much improved. It would be unreasonable to expect today’s 65-year-olds to work manual labor for a living, but office jobs are far more common today than they were in 1935. Even with an aging body, 65-year-olds can and do make a good living sitting at a desk. For those who have lost the physical ability to work at that age, the Social Security Disability Insurance program is there to help.

To avoid an ever-growing government debt burden, Social Security’s retirement age should probably rise as the life expectancy of its recipients rises.