There’s another universe where President Joe Biden signs his so-called Inflation Reduction Act into law, but in March 2021 — when inflation was 2.6%, rather than approaching double digits.

The San Francisco Fed estimates that Biden’s $1.9 trillion American Rescue Plan caused more than half of last year’s inflation. This new bill modestly reduces the annual multitrillion-dollar deficit by $300 billion through 2031. Had this been tried instead of the American Rescue Plan, perhaps that would have offset inflation. Not only would it have cut into the sizable costs of our interest on federal debt (which will consume nearly 40% of our federal revenue by 2051), but it would have also sent a clear signal that we’d be returning to normal levels of demand — no need for massive additional spending.

Beyond the political implications of siccing the IRS on the middle class (or whatever other partisan reasons Republicans give for opposing this bill), its real problem is that it is not an inflation reduction act at all. It is a deficit-reducing social spending bill that cannot reduce inflation in any meaningful way.

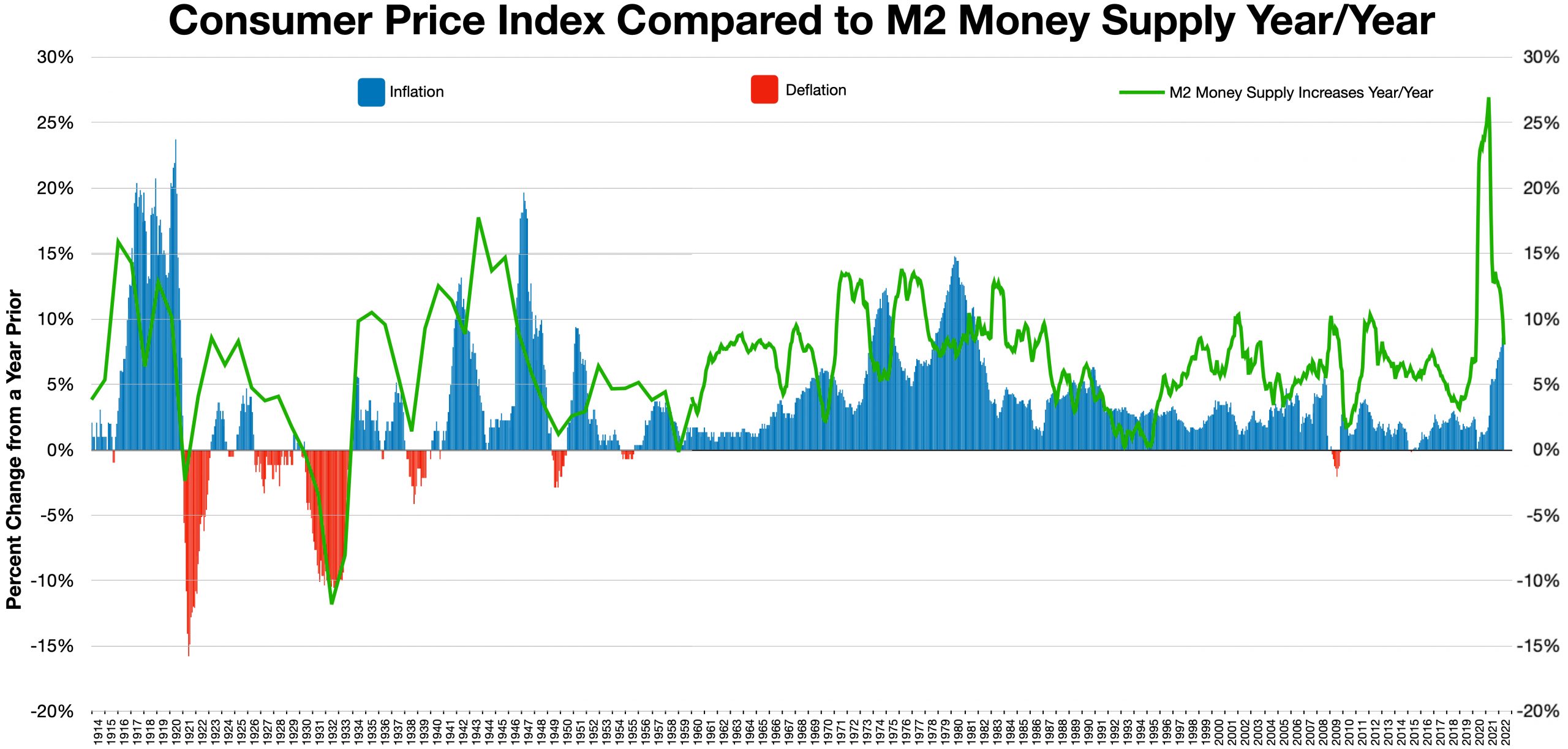

Let’s recap some elementary macroeconomics. Despite the collective amnesia of the Fed, the Hill, and the rest of the financial establishment over the past decade, inflation is a monetary phenomenon. The formula may not be exact, but since the inception of the Fed, irregular and elevated expansion of the money supply has always preceded bad bouts of inflation.

So now, let’s dial into the past quarter-century. From 1998 to 2008, the M2 money supply grew by $3.5 trillion. From the beginning of the quantitative easing experiment to the coronavirus achieving pandemic status, the money supply grew by $8 trillion. From March 2020 to the start of this year, the Fed added $6 trillion to the money supply, or nearly 30% of all dollars currently in circulation.

In that context, a reduction of tens of billions from the annual deficit means little. More importantly, the Keynesian guidebook is poorly equipped to handle our current morass of stagflation. John Maynard Keynes prescribed the use of fiscal policy to spend against the wind — that is, to have government run deficits to induce demand during recessions and then save to curb demand during inflation. But our economy is both too hot and too cold for this to work. That is, inflation has run so high as to stunt output.

It would be political suicide to raise taxes to the point that it actually contracts the money supply. That’s why the Fed’s role is crucial. And thus, we’re beholden to unelected (and for now apparently too timid) bureaucrats who spent the last 10 years convincing themselves that keeping interest rates near zero during the longest bull run in history wouldn’t create unprecedented asset price inflation.

Congress’s actions are so contradictory as of late that the real cost of the Inflation Reduction Act on the public is impossible to predict. The act will force Tesla to pay a 15% corporate minimum tax while offering a boon to Tesla with the electric vehicle tax credit. About half of the corporate minimum tax’s burden will be borne by the manufacturing sector, which also just a week earlier got a multibillion-dollar payday from Congress in the form of the CHIPS Act.

As a political body, Congress just wants to keep spending and make people happy. That’s why it’s left to the Fed to dole out the tough medicine to curb inflation. The only question is whether Jerome Powell has the guts to step up and do what Congress cannot and will not.