The rapidly escalating conflict in Iran is already sending shockwaves through commodities markets, including aluminum — a strategic industrial material essential to civilian and military uses that the U.S. still largely sources from abroad. It’s a stark reminder of how quickly geopolitical instability can expose strategic vulnerabilities at home.

Against that backdrop, January’s announcement of a new aluminum smelter in Oklahoma, the first new facility built in the United States in nearly half a century, represents an enormous milestone. Once an energy deal is secured from the state, the project will double the current domestic primary aluminum production.

Recommended Stories

But it’s not nearly enough.

THE COPPER CRISIS: OVERCAPACITY IN CHINA AND UNDERINVESTMENT IN AMERICA

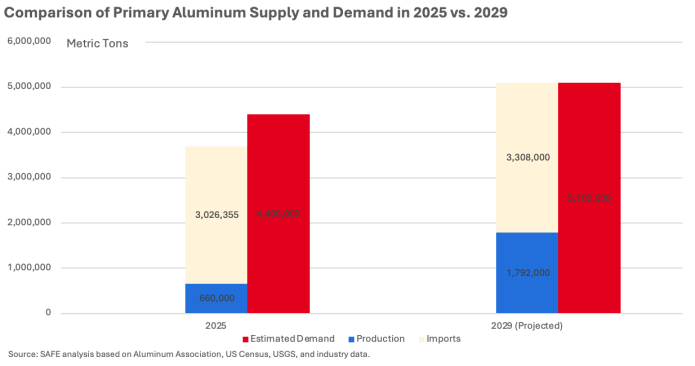

Current domestic primary aluminum smelters produced about 16% of the needed supply. The new globally competitive smelter will only enable the U.S. to supply just 25% of projected demand by 2029, when the new plant is expected to come online. Fully 75% of aluminum supplies will still have to come from foreign sources, and the U.S. will be exposed to all the risks and volatility that come with that — as we’ve seen most recently with Iran.

Though in our globalized world it may not be reasonable to expect the U.S. to supply 100% of our own aluminum, even achieving 50% domestic supply — a level that would meaningfully strengthen supply-chain security — would require not just one, not just two, not just three, but four more Oklahoma-scale smelters. Addressing the scale of the issue requires thinking bigger than our current metals policy allows.

Our dependence on aluminum is not theoretical. A steady, reliable supply of aluminum is a national security and economic imperative. The Department of War relies on aluminum for aircraft, armored vehicles, satellites, communications equipment, and munitions. The electrical grid depends on aluminum for long-distance, high-voltage transmission because it is lighter, cheaper, and more efficient than alternatives. Transportation alone accounts for a significant share of U.S. aluminum consumption, with the average North American vehicle now containing nearly 460 pounds of aluminum, up sharply over the past decade.

These strategic needs cannot be filled by just any kind of aluminum, nor can they be supplied reliably on a just-in-time basis from abroad. Defense and aerospace systems often require high-purity primary aluminum produced to exacting specifications. Secondary aluminum made from recycled scrap plays a critical role in vehicles and infrastructure. Both are increasingly vulnerable to supply disruption.

The problem begins upstream. Alumina, the refined form of bauxite used to make primary aluminum, has seen domestic production collapse. The U.S. now has a single operating alumina refinery, creating a dangerous single point of failure. Meanwhile, China — backed by state subsidies and unconstrained by market discipline — has built massive overcapacity, flooding global markets and depressing prices in ways that undermine remaining U.S. producers.

Primary aluminum production tells a similar story. Once the world’s leading producer, the U.S. has fallen well behind other countries. Just four smelters remain, operated by two companies, operating at less than full capacity last year. The core challenge is energy. Smelting aluminum requires a constant, uninterrupted flow of electricity, with power costs accounting for up to 40% of total production costs. Volatile energy prices and short-term contracts make long-term investment nearly impossible.

In many ways, energy is nearly the entire story. China’s dominance is inseparable from energy policy. Roughly 80% of Chinese smelters are coal-powered and benefit from opaque, state-backed energy subsidies that insulate producers from market signals. The result is chronic overproduction, suppressed global prices, and rising U.S. dependence on imports for critical infrastructure and military needs.

Recycling helps, but it is not a panacea. Secondary aluminum cannot substitute for primary metal in many defense and aerospace applications, and there is simply not enough scrap to meet rising demand. Compounding the problem, the U.S. exports more than twice as much aluminum scrap as it produces in primary metal, effectively feeding foreign defense industrial bases, especially China’s.

Stockpiling alone cannot solve these challenges. Recent conflicts in Ukraine and the Middle East have demonstrated how quickly reserves can be depleted and how difficult it is to surge production without stable supply chains and long-term contracts.

TRUMP SAYS LEAVING ‘PAPER TIGER’ NATO IS NOW ‘BEYOND RECONSIDERATION’

If the U.S. is serious about rebuilding its defense industrial base, it must start with materials. That means stabilizing energy costs, investing in domestic processing capacity, prioritizing U.S.-sourced aluminum in defense procurement, treating aluminum scrap as a strategic asset, and forming durable public-private partnerships that reward long-term production, not short-term arbitrage.

Losing the ability to make our own aluminum will cost us our resilience, deterrence capabilities, and strategic autonomy at a moment when the nation can least afford it.

Joe Quinn is executive director of the SAFE Center for Strategic Industrial Materials and an adviser to the Forging the Future coalition.